Between a Rock and a Hard Place

Between a Rock and a Hard Place

Analyzing the relationship between ETH as a deflationary asset and the scalability of the Ethereum Blockchain

Hey everyone! Hope y’all had a great New Year’s celebration! I took last week off from writing a blog for two reasons:

I went to Dallas to watch my alma mater Tulane play USC in the Cotton Bowl. Let me tell you, it was one of the greatest sports moments of my life! Objectively one of the craziest comebacks I’ve ever seen. Here are a few clips and tweets to show how incredible it was.

Besides the notorious “No Call” Saints game, this was probably the most memorable sports fan moment of my life. The amount of Tulane people who showed up was incredible as well, and it was fun reconnecting with so many people I haven’t seen in a few months.

This past Sunday, I started the 12 Cities, 12 Months journey that I mentioned in my last blog, which had by far been my most read one. I’ve had so many people come up to me and mention how they love my blog and this idea in the past week or so that I’m honestly shocked. Maybe it was because I didn’t write about Web 3.0 for once, so people were actually interested in it, but I’ll just tell myself that it was because I wrote such an amazing blog instead. I’m currently writing this in a Starbucks in Tampa, so if you have any recommendations on what I should go see, do, eat, etc. please let me know. Also, if you want to follow along on my journey, you can check out all my social links here.

Now, let’s get onto the blog.

Ethereum is touted by many as the premier blockchain in the cryptocurrency ecosystem due to having the most TVL of any blockchain, the most volume, the largest developer community, the best projects and applications being built on top of it, and more. Even top projects from other ecosystems are switching to Ethereum. For the most part, I agree with this take as it's hard to argue against the blockchain’s success.

However, there are two big narratives around the Ethereum ecosystem that I haven’t yet been able to get my head around as they seem to directly contrast one another:

Ethereum is a deflationary asset due to the fee burn created by EIP 1559 and increased with the Merge

Ethereum lowering its fee costs with scalability improvements like sharding and increased usage of L2s

To help sort out this conundrum in my head, I figured I’d write a blog analyzing the two of them and see if we could find a conclusion. This may be a little more technical than some of my other blogs, but hopefully, I can make it clear for anyone reading who may be new to this stuff.

ETH Deflationary Asset

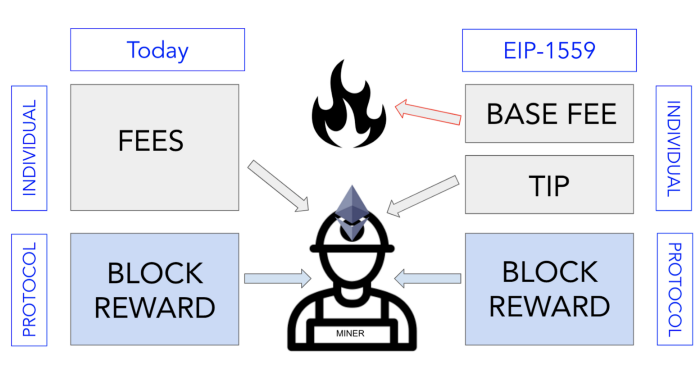

The first step to understanding how ETH is a deflationary asset is to look at Ethereum Improvement Proposal (EIP) 1559. Executed on August 5, 2021, this improvement made it so that a portion of the gas fees paid by users would be burned (aka, destroyed) instead of going to PoW miners.

Before this improvement, ETH was structurally set up as an inflationary asset that would always increase in supply over time. However, with this new upgrade, the possibility of ETH becoming deflationary existed as long as “daily fee burns…exceed the daily rewards paid out to miners.” However, the likelihood of this was highly unlikely as gas fees (transaction costs) would need to remain at a sustained 150 gwei which, for any non-crypto natives here, is ridiculously high.

However, the Ethereum Merge changed this whole dynamic. Before the merge, PoW miners were issued 13,000 ETH/day for their work helping secure the Ethereum blockchain, resulting in an annual inflation rate of about 4%.

After the Merge, the miners’ replacement, stakers, receive about 1,700 ETH/day to help secure the network, resulting in about a .52% issuance rate (about an 89% reduction compared to PoW).

This means EIP 1559’s burn has a much greater effect as there is simply less ETH available to burn. Thus, the required sustained gwei needed to become deflationary is also significantly reduced, being at around 16–17 gwei at the time of writing.

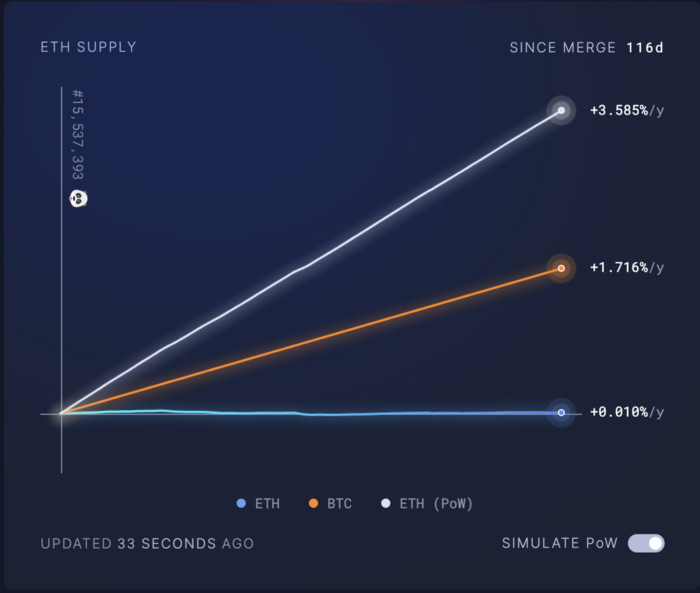

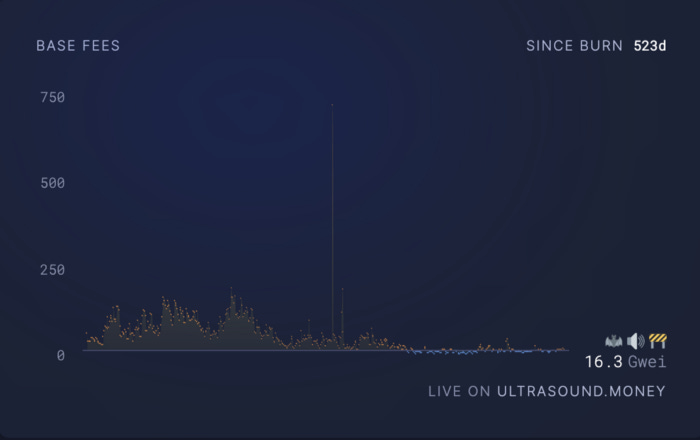

The website Ultrasound.money does a great job showing the impact that EIP 1559 and the Merge have on ETH as a deflationary asset. The craziest stat the website shows in my opinion is the difference in the issuance of ETH now vs. if it was still a PoW blockchain. There has been an increase of about 3,500 ETH to the total supply since the merge to PoS took place. If PoW was still in place, that number would be almost 1.4 million ETH.

ETH Scalability

One of the biggest gripes that people have had with the Ethereum blockchain is its scalability issue. Although Ethereum, as mentioned earlier, is touted as the best smart contract blockchain due to the myriad of reasons mentioned above, criticizers frequently point to Ethereum's expensive transaction fees, low number of transactions per second (about 15), long block times, and more.

These issues led to the rise and growth of what is known as “ETH Killers” or alt-L1s, which are other blockchains that prioritize faster and cheaper transactions to possibly take away some of Ethereum’s market share. Some examples include Solana, Near, Polkadot, Avalanche, Cosmos, and more.

However, Ethereum developers have already started countering this rise in competition with developments of their own:

Layer 2 Blockchains

Protodanksharding

Layer 2s

Layer 2 solutions (L2s) are the most prevalent and popular scaling solution on Ethereum today as they require no changes to the existing Ethereum protocol due to how much easier they are to implement than protocol level changes (the Merge took multiple years for reference).

Generally speaking, an L2 on Ethereum is a separate blockchain that extends Ethereum while still inheriting the same security guarantees of Ethereum itself. I know that’s probably confusing to some of my less crypto-inept readers, but keep with me. Instead of having to pay transaction fees for each transaction, an L2 bundles all these transactions together and execute them outside Ethereum, but receive the same security guarantees by posting proof that these transactions took place on Ethereum.

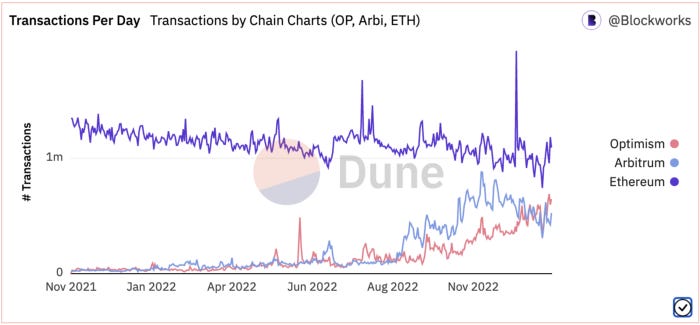

There are more and more L2 popping up every single week, especially with the rise of zero-knowledge rollups, but some of the more well-known L2s include more generalized solutions like Arbitrum and Optimism and application-specific solutions such as Immutable X, Aztec, and more.

Sharding

Unlike L2s, sharding would change the Ethereum protocol itself to make the blockchain more scalable. It’s a very common core principle in computer science, but the Ethereum team is looking to replicate it to their blockchain in their own way.

Sharding simply refers to splitting a blockchain into smaller portions to enhance overall efficiency. For instance, instead of processing a transaction worth $1,000,000 on Ethereum, the transaction can be broken down into 100 shards, each bearing $10,000 worth of transactions.

In Ethereum’s case, “sharding will work synergistically with layer 2 rollups by splitting up the burden of handling the large amount of data needed by rollups over the entire network.” This would reduce the congestion on the Ethereum overall, while also improving the speed of the network, increasing storage capabilities, and reducing fees.

The Ethereum core developer team is planning on implementing their particular version of this improvement called proto-danksharding (I know, weird name, but it’s named after two developers), which is expected to be shipped at the later end of 2023. Since this is a super complex & technical topic, I know that I am in no way, shape, or form qualified to explain it, so you can refer to this link from Alchemy (premier blockchain company) if you want to learn more.

Conflict of Interest and Potential Solution

Hopefully, you can now start to see a contrast between these two dominating Ethereum narratives: ETH can become a deflationary asset if the Ethereum network can keep a sustained gas fee while at the same time, Ethereum developers are looking to improve overall network scalability through L2s and sharding, which will inherently make transactions cheaper, thus reducing gas fees. It’s like two rams in the wild butting heads with one another to see which will win out.

So how could ETH become a deflationary asset while also creating a more scalable Ethereum blockchain? Again, I am far from being an expert, and still am trying to find a good answer to this question myself (I’ve been asking in almost every Discord group I am a part of) but I have a few ideas:

The first and easiest way for both to co-exist with one another would be to increase the number of users both on the Ethereum L1 itself and L2 solutions. The more people that are using the Ethereum blockchain, the more demand there is for Ethereum block space, thus causing higher gas fees and more ETH burn. With enough users, at some point, there should easily be enough transaction demand to hit the 15–17 gwei required for ETH to become deflationary as that number is still significantly lower than pre-merge.

Another way ETH could become deflationary while also having Ethereum become a more scalable blockchain may simply come down to spurring another bull market. During a bull market, people make more money in crypto, which also makes them more inclined to spend money through gas fees on-chain as each transaction represents a smaller percentage of overall net worth. Although creating a bull market is not simply something that happens with the flip of a switch, it would definitely make it a world where the two narratives could co-exist with one another. Check out the stark contrast in gas fees during the bear market vs. the current bull market from the graph below.

The clear (and kinda big) assumption I’m making here is that the scalability improvements would not be big enough so that previously sustained 100+ gwei market activity would not drop to under 15–17 gwei. If the improvements do surpass my expectations (which I am not basing on much since I do not know the impact that scalability improvements will have), the hope is that cheaper transactions would spur more people to join the network, which would in turn spur more market activity.

Because I realize I’m not even close to being the brightest person involved in this industry, I reached out to the Ethereum R&D Discord server, which has some of the best and brightest Ethereum minds to see what they said. Here’s a response I got from Jesse Pollak, a Senior Director of Engineering at Coinbase:

Regardless, the most important thing is that builders in the crypto ecosystem need to create more projects, applications, and killer use cases that are useful to current & new users alike. Just like most problems currently facing the crypto market, most of them can be solved by building useful tools that help people understand the impact and power of blockchain technology. With less noise and hype around the price of things going up, hopefully, 2023 can be a year to focus on building the industry up for a better & brighter future.

Links used if you want to learn more (links also included throughout the blog):

Ultrasound.money (amazing tool; keep open on my browser 24/7)

Don’t know what I’ll write about next week yet, but I’ll be exploring Tampa for the rest of this week. If anyone has any recs, please let me know!

Here are my links if you feel inclined: